Work Related Expenses – Car Use

Author Alan Maddick 12th November 2021

You can download this article in Pdf format here

Preparing Tax Returns and talking to people about Tax inevitably the subject of “what can I claim?” comes up. What people typically mean by this is what work related expense (often called WRE in the industry) can I claim on my tax return to decrease my taxable income and so increase my tax refund. Tax is confusing and discussion of work related expenses is no different but lets have a bit of a look at what you can claim. In this paper I will attempt to explain car related claims and where the laws and practices we use come from.

There are 3 main areas that tax laws come from;

- Legislation – the laws that are written by politicians that as Australians we all need to follow.

- Case Law – some law comes from court cases, they may be old cases about fundamental principals for example what is income and what is capital has been discussed and decided by the courts over many years (200 years or more dating back to UK cases) or else where legislation is not clear the courts may resolve a difference of opinion between the ATO and a Taxpayer.

- The ATO – the ATO is responsible for enforcing the law but they are technically not the source of the law. However they are a source of information, some of the information they issue is what is called a ruling and other forms are general administrative guidance and published articles.

Preparing a tax return

This is article is only about Individual Tax Returns; the rules for other tax returns like Companies and Trusts is different. When we prepare tax returns as Accountants we put your Work Related claims (and actually all your data) into specific boxes on your tax return form which is then submitted to the Australian Tax Office

In the case of Work Related Expenses the boxes in question are D1 – D5. These boxes and what goes in them is set by the Commissioner of Taxation, section 161A of the old 1936 Tax Act gives him this ability.[1] Unless you want a fine you need to follow these instructions.

The underlying law about what you can claim and cannot claim does not stipulate what box you need to put it in, this is an example of something the Commissioner establishes via his power to administer the Tax Legislation. Lets have a look at the main sections and common claims and issues and where these rules are coming from.

Car D1

The ability to claim tax deductions in general is set out in section 8-1 of the 1997 tax legislation:

“8-1(1) You can deduct from your assessable income any loss or outgoing to the extent that:

(a) it is incurred in gaining or producing your assessable income;…”[2]

This seems simple but it gets more complex from there, in the case of Cars firstly you need to be clear about what is a car – Car claims go in the first of Deductions boxes on the Individual tax form (D1). Car tax deductions have their own division of the 1997 Tax Legislation, division 28[3].

A car is defined as: “car means a *motor vehicle (except a motor cycle or similar vehicle) designed to carry a load of less than 1 tonne and fewer than 9 passengers.”[4]

This same division of the Tax Laws also sets out special rules for tax deductions for cars:

28-12(2) You must use one of the 2 methods unless an exception applies. If you can’t use either of the methods, you can’t deduct anything for the *car expenses.

*[5]

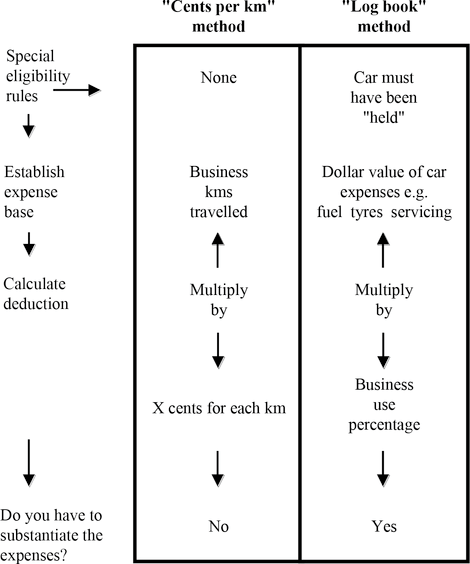

- Log Book Method

Section 28F of the 1997 tax legislation[6] sets out the rules for the Log Book Method, on of the first and important points about using this method is “you can use this method only if you * held the * car for some or all of the income year.”[7] What this means is you need to own the car, seems simple enough but for example you might be driving your husband’s car for work, in this case you cannot use the log book method.

As long as you held the car and used it for business purposes you will be able claim your actual car costs, you will need to substantiate these with tax invoices. (actual costs are things like petrol, servicing and other direct costs)

You can only claim the percentage of actual car costs that are business related, you work this out by keeping a log book.[8] You need to keep a log book which records you business and private trips for a period of 12 weeks,[9] once you keep this log book in a given year it can be used for another four years so it can be used for five years in total.[10]

You can claim for using 2 cars for work but in this case you will need to keep one log book for each car that over the same 12 week period.[11]

- C/km

The cents per kilometre method is quite simple for each business kilometre travelled you get a certain number of cents of tax deduction. The current rate is 72c per km but it does vary from year to year. Business kilometres are defined as:

“ Business kilometres are kilometres the *car travelled in the course of:

(a) producing your assessable income; or

(b) your *travel between workplaces.

You calculate the number of business kilometres by making a reasonable estimate.”[12]

- Others – there were other methods to claim car expenses but they are no longer available.

Because Car claims are common and can be quite high there are a large number of court cases that relate to them. Some examples of issues that have been resolved by the court:

- A tax payer claimed $10,310 for car use based on a log book he had kept, there were some issues about the way this was completed but the main issue was that he was buying the car using a hire purchase loan agreement. The terms of this agreement meant that he would not own the car until the end of the agreement, because this meant he did not hold the car his tax deduction was thrown out.[13]

- At tax payer tried to claim that his home was his base of employment and so he could claim travel from home to work. In this case there was no basis for this other than he conducted minor office type tasks at home before leaving for work.[14] 79 ATC 339 is also very similar to this.[15]

D2 Travel

At this box of the tax form we claim what you would commonly think of as travel for example airfares and hotels but we also claim a range of what many people would think of as car expenses:

- Parking fees

Parking fees are contentious as many people feel if they have to park at work this should be a tax deduction. The issue is that travel to and for your normal place of work is not deductible and so parking when you are at work is generally taken to be private in nature on the same basis.

There are a couple of notable cases that further confirm this in the first case a university lecturer was disallowed fees paid for parking within the university grounds on the basis that they formed part of the private cost of travelling between home and work[16]. In a second case a sales representative’s parking fees were deductible[17] the difference between the cases is that the University lecturer was parking at his normal place of work where the sales representative incurred parking fees when parking on sales calls and so this cost was “incurred in gaining or producing [his] assessable income”[18]

- Taxi and Uber fares

- Tolls, as long as you are re-imbursed for these costs you can claim them if they are incurred on a business or work related trip.

- Costs of vehicles that are not cars. Only cars are covered by the special rules of Division 28 we talked about earlier. Vehicles that are not cars are not captured by these sections and their special rules about making claims (log books and c/km methods). Typical vehicles that would be included here are Motor Cycles, Utes and Vans that can carry over 1 tonne as well as heavy commercial vehicles.

As the special deduction rules in division 28 do not apply to these vehicles you only need to meet the basic test in section 8-1

“8-1(1) You can deduct from your assessable income any loss or outgoing to the extent that:

(a) it is incurred in gaining or producing your assessable income;…”[19]

From this it seems that as long as you use your vehicle in generating assessable income you can claim it, but s 8-1 contains a second negative limb which states that:

“8-1(2) However, you cannot deduct a loss or outgoing under this section to the extent that:

…(b) it is a loss or outgoing of a private or domestic nature;…”[20]

What this means is that where a deduction is used to generate assessable income and also has a private or domestic nature you need to apportion the amounts between work related and private. Unlike the prescriptive rules for car deductions we discussed earlier there is not prescribed way to do this apportionment, but please be aware in an audit situation you will need to prove your apportionment is reasonable and fair.

Conclusion

Hopefully that gives you some insight into what you can and cannot claim in relation to car use on your tax return and where these rules come from. If you want some advice or assistance with your Work Related Expense issue please get in contact.

Alan Maddick MFP, Grad Dip App Fin, Fellow IPA,

[1] Income Tax Assessment Act 1936, Cth, s 161A

[2] Income Tax Assessment Act 1997, Cth s 8-1

[3] Income Tax Assessment Act 1997, Cth s 28 onwards.

[4] Income Tax Assessment Act 1997, Cth s 955-1

[5] Income Tax Assessment Act 1997, Cth s 28-15

[6] Income Tax Assessment Act 1997, Cth s 28F

[7] Income Tax Assessment Act 1997, Cth s 28-95

[8] Income Tax Assessment Act 1997, Cth s 28-105

[9] Income Tax Assessment Act 1997, Cth s 28-110

[10] Income Tax Assessment Act 1997, Cth s 28-115

[11] Income Tax Assessment Act 1997, Cth s 28-120(3)

[12] Income Tax Assessment Act 1997, Cth 28-25(3)

[13] Case 49/94, Administrative Appeals Tribunal of Australia, 21 September 1994 94 ATC 429

[14] Case K5, Board of Review No. 1 (Australian Taxation Board of Review No1), 17 February 1978 78 ATC 51

[15] Case L49, Board of Review No. 3 (Australian Taxation Board of Review No3), 31 August 1979 79 ATC 339

[16] Case C47, 71 ATC 219

[17] Case Y43, 91 ATC 412

[18] Income Tax Assessment Act 1997, Cth s 8-1

[19] Income Tax Assessment Act 1997, Cth s 8-1

[20] Income Tax Assessment Act 1997, Cth s 8-1(2)(b)